|

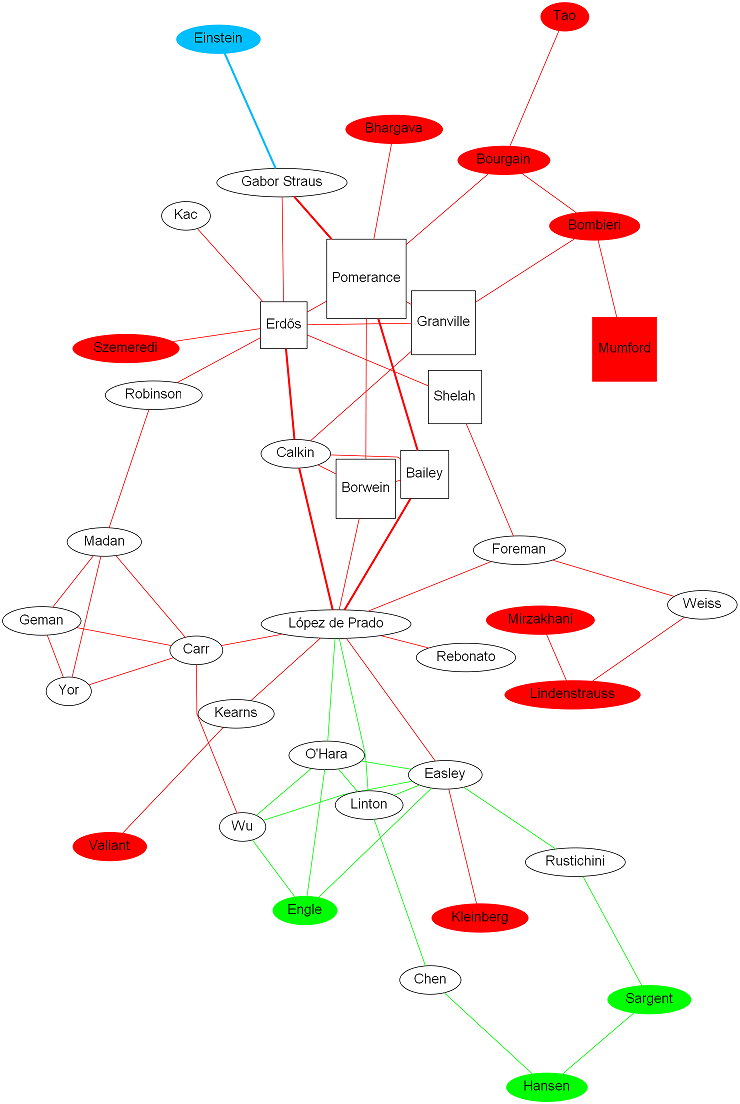

An author collaboration network. [Source: American Mathematical Society, SSRN] |

COLLABORATION NETWORK

Below is a summarized collaboration network, which makes it easy to visualize three main clusters: Pure Mathematics (centered around Paul Erdős and the Fields-Nevanlinna medallists), Mathematical Finance (centered around the Carr-Geman-Madan-Yor team) and Financial Econometrics (centered around the Nobel Laureates in Economics).

|

An author collaboration network. [Source: American Mathematical Society, SSRN] |

Contrary to common belief, modern mathematical research is a highly collaborative enterprise, where teams of researchers pursue a common interest and build upon each others' innovations. A formalized field lends itself to team-working because concepts can be rigorously defined and debated (see the Polymath project for astonishing examples of massive collaboration).

CO-AUTHORS

Below is a partial list (in alphabetic order) of the ~50 co-authors with whom I have had the fortune to do research and publish some of our results.

| NAME | FIELD | PUBLICATIONS | COMMENTS |

| Dr. Robert Almgren |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Alexander Antonov | Pricing | [1], [2] |

|

| Dr. David H. Bailey |

Experimental Mathematics Computational Research Mathematical Finance |

[1], [2], [3], [4], [5], [6], [7], [8], [9], [10], [11], [12], [13], [14], [15], [16], [17], [18], [19] |

|

| Dr. Wes Bethel | Computer Science | [1] |

|

|

Dr. Jonathan M. Borwein, FAMS, FRSC, FAAAS, FBAS, FAA |

Variational Analysis Computational Research Mathematical Finance |

[1], [2], [3], [4], [5], [6], [7], [8] |

|

| Dr. Stephen P. Boyd |

Convex optimization Stochastic Control Dynamical Systems |

[1] |

|

| Dr. Neil J. Calkin |

Graph Theory Combinatorial Methods Number Theory |

[1], [2] |

|

| Dr. Peter P. Carr |

Mathematical Finance Stochastic Processes Optimal Control |

[1], [2] |

|

| Dr. Mark Coeckelbergh | Trustworthy AI | [1] |

|

| Dr. David A. Easley |

Market Microstructure High Frequency Trading Computer Science |

[1], [2], [3], [4], [5], [6], [7], [8], [9], [10] |

|

| Dr. Robert F. Engle | Econometrics | [1] |

|

| Dr. Frank Fabozzi | Mathematical Finance | [1], [2], [3], [4], [5], [6], [7] |

|

| Dr. Matthew D. Foreman |

Set Theory Mathematical Finance |

[1] |

|

| Dr. Phil Goddard |

Quantum Physics Quantum Computing |

[1] |

|

| Dr. Ming Gu | Optimization and Numerical Methods | [1] |

|

| Dr. Terry Hendershott |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Miguel Hernán | Causal Inference | [1] |

|

| Dr. Enrique Herrera | Trustworthy AI | [1], [2], [3] |

|

| Dr. Francisco Herrera | Trustworthy AI | [1], [2], [3], [4], [5], [6] |

|

| Dr. Guido Imbens | Causal Inference | [1] |

|

| Dr. Charles Jones |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Michael Kearns |

Machine Learning High Frequency Trading Operations Research |

[1] |

|

| Dr. David J. Leinweber |

Machine Learning Mathematical Finance |

[1], [2] |

|

| Dr. Oliver Linton, FBA |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Alexander Lipton | Mathematical Finance | [1], [2], [3], [4], [5], [6], [7], [8] |

|

| Dr. Albert Menkveld |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Yuryi Nevmyvaka |

Machine Learning High Frequency Trading Operations Research |

[1] |

|

| Dr. Richard Olsen |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Maureen O'Hara |

Market Microstructure High Frequency Trading |

[1], [2], [3], [4], [5], [6], [7], [8], [9], [10] |

|

| Dr. Achim Peijan | Mathematical Finance | [1] |

|

| Dr. Eva del Pozo | Mathematical Finance | [1] |

|

| Dr. Riccardo Rebonato | Mathematical Finance | [1], [2] |

|

| Dr. Oliver Ruebel | Computer Science | [1] |

|

| Dr. Horst Simon |

Computer Science Supercomputing Algorithms |

[1], [2], [3], [4] |

|

| Dr. George Sofianos |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Michael Sotiropoulos |

Market Microstructure High Frequency Trading |

[1] |

|

| Ralph Vince |

Computer Science Game Theory |

[1] |

|

| Dr. Fei-Yue Wang | Computer Science | [1] |

|

| Dr. Kesheng Wu | Computer Science | [1], [2], [3], [4], [5], [6], [7] |

|

| Dr. Jim Zhu |

Variational Analysis Computational Research Mathematical Finance |

[1], [2], [3], [4], [5], [6] |

|

| Dr. Jean-Pierre Zigrand |

Market Microstructure High Frequency Trading |

[1] |

|

| Dr. Vincent Zoonekynd |

Causal Inference Factor Investing |

[1], [2], [3] |

|